Patrick McHenry, chairman of the US House Financial Services Committee (FSC), announced a handful of bills, including three that seek regulatory clarity for the digital asset ecosystem: crypto, blockchain development, and stablecoin payments.

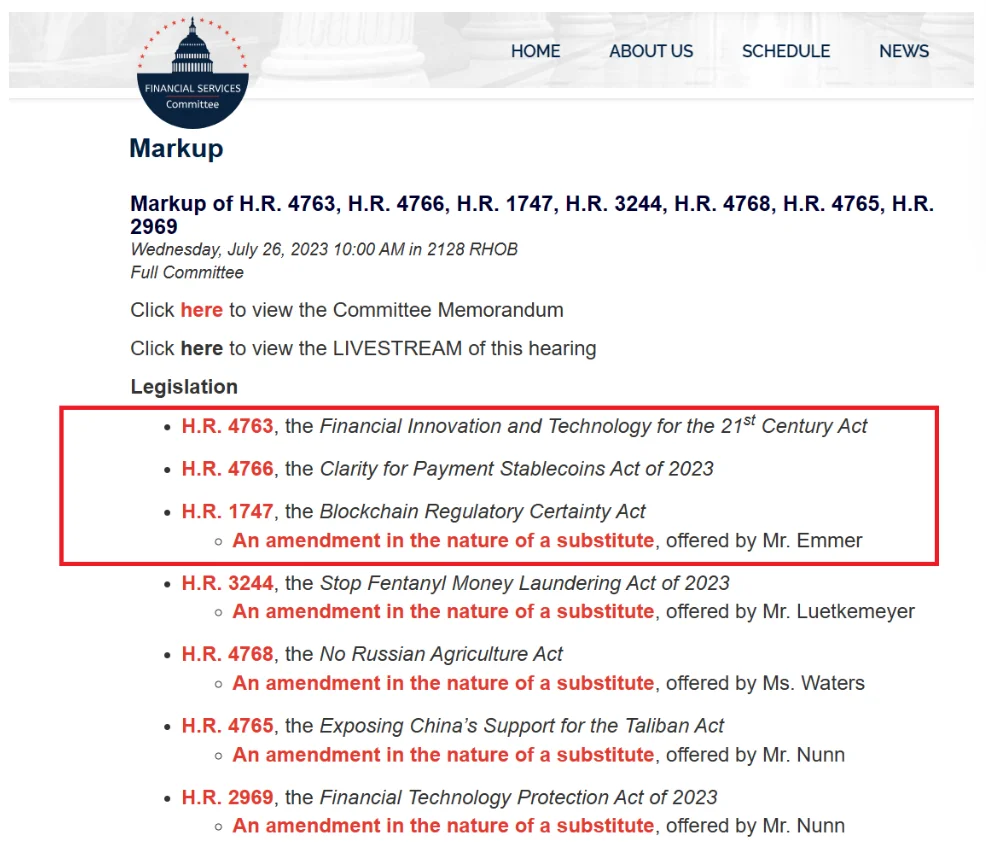

On July 26, the Committee on Financial Services will markup, among other bills, H.R. 4763, the Financial Innovation and Technology for the 21st Century Act, H.R. 4766, the Clarity for Payment Stablecoins Act of 2023, and H.R. 1747, the Blockchain Regulatory Certainty Act.

McHenry introduced the markup on clarity for stablecoin payments, which seeks to provide regulatory clarity for issuing stablecoins intended for use as a means of payment.

As stated in the memorandum issued on July 21, H.R. 4763 establishes a market structure framework for digital assets appropriate for their unique characteristics. H.R. 1747 eliminates the need for blockchain developers to obtain licenses if they do not engage in cryptocurrency trading.

The markup date was declared the day after the Financial Innovation and Technology for the 21st Century Act was introduced. According to U.S. Representative French Hill, who serves as chairman of the Subcommittee on Digital Assets, establishing a functional regulatory framework protects investors from financial fraud.

“This legislation not only would have prevented FTX from stealing billions of dollars in customer funds, but it also establishes robust consumer protections and clear road rules for market participants,” he added.

The Department of Justice (DoJ) of the United States decided to double the size of its crypto crime team.

The Computer Crime and Intellectual Property Section (CCIPS) and the National Cryptocurrency Enforcement Team (NCET) will consolidate to form a larger organization with more resources.

The number of criminal division attorneys available to work on criminal cryptocurrency matters will “double,” as any CCIPS attorney could potentially be assigned to an NCET case.