Since January 2024, cryptocurrency wallets associated with the defunct FTX exchange and its subsidiary, Alameda Research, have transferred over $38.8 million of digital assets to multiple other cryptocurrency exchanges.

Wallets affiliated with both organizations transferred a minimum of $7 million to exchanges in February, according to data tracking by blockchain analytics firm PeckShield.

On February 4, the addresses transferred approximately $1.1 million in Ton (TON) and Fantom to FalconX and Wintermute and $2.6 million in Ether to Coinbase. Coinbase, Coinbase Prime, FalconX, and Binance received a minimum of $3.3 million worth of assets from the cryptocurrency wallet addresses on February 6.

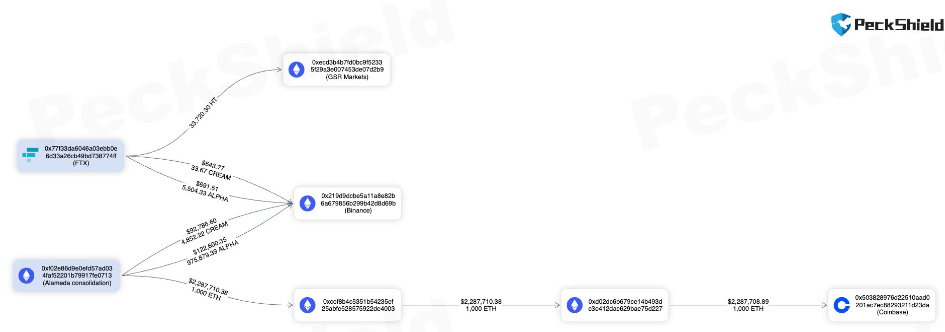

The cryptocurrency wallets associated with FTX and Alameda transferred a minimum of $35 million to exchanges in January. The wallets transferred $4.1 million in Cronos to Coinbase on January 4. On January 9, the accounts transferred $2.4 million in ETH to Coinbase and 200 Wrapped BTC (WBTC) to Binance for $9 million.

FTX and Alameda transferred an additional $16.3 million to multiple exchanges later in January. Addresses associated with the organizations moved $2.6 million in ETH to Wintermute and $8.9 million in Tether Gold (XAUT) to Coinbase on January 17.

The crypto addresses subsequently transferred $1.3 million in various altcoins to Binance, $2.3 million in ETH to Coinbase, and $1.28 million to GSR Markets on January 30.

Fund movements occurred amid the defunct exchange's reorganization initiatives and the disclosure of its intentions to reimburse its customers. In a U.S. court hearing on January 31, the defunct exchange stated that its reorganization objectives would not involve re-establishing the exchange but rather the complete repayment of its customers. Andy Dietderich, an attorney for FTX, noted that customer repayment was merely an objective and not a guarantee.

In the wake of the hearing, the restructuring plan was subject to criticism, with some highlighting the financial gains achieved by the legal team during the ordeal. John Reed Stark, a former United States Securities and Exchange Commission official, characterized the scheme on February 4 as a “highway robbery of highway robbers.”