DeFi, or decentralized finance, has emerged as a transformative force in the rapidly evolving finance landscape. This article explores the basics of DeFi lending and borrowing, shedding light on the decentralized platforms revolutionizing traditional financial practices.

What is DeFi lending and borrowing?

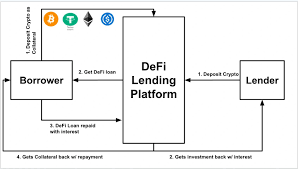

DeFi lending involves users supplying their digital assets to earn interest, while DeFi borrowing allows users to borrow assets by providing collateral.

These activities contribute to the broader concept of decentralized finance, aiming to create more accessible and inclusive financial services.

DeFi lending and borrowing operates on the principles of decentralization, utilizing smart contracts and blockchain technology to facilitate secure and transparent lending and borrowing.

Unlike traditional borrowing and lending, DeFi lending and borrowing eliminates the need for intermediaries, providing users with greater control over their assets.

Why Borrow and Lend In DeFi?

Lending and borrowing in DeFi offers many benefits that centralized finance options can’t. Some of the most important benefits of DeFi lending and borrowing include much higher efficiency, access, and transparency in the process than CeFi.

DeFi also allows people to become borrowers or lenders without having to hand over personal information for KYC (know your client) requirements and procedures.

Also, in the case of DeFi, borrowers and lenders do not have to hand over the custody of their funds, as is the case with CeFi. In other words, the user can always get to their money. Smart contracts that run on open-source blockchain networks like Ethereum make this possible.

How Does Lending and Borrowing work in DeFi

Smart contracts allow users with spare cash to pool it and then distribute it to borrowers.

Simply said, smart contracts are rules-based computer codes that execute on the blockchain.

There are several ways of allocating interests to investors; as a result, you should take the time to learn about your interest type. Similarly, each pool will use a slightly different approach to borrowing.

DeFi lending and borrowing are similar to traditional borrowing in some ways, however.

Borrowing money from a bank usually requires putting up some sort of collateral. For instance, if the borrower cannot repay a car loan, the bank may take the vehicle as collateral and sell it to cover the debt.

Decentralized systems work on the same principle; the main distinction is that they are digital and autonomous, eliminating the need to use physical assets as collateral. To secure a loan, the applicant must pledge an asset valued higher than the loan amount.

You can use one cryptocurrency as collateral to borrow another cryptocurrency. One could borrow one bitcoin by paying the equivalent of a bitcoin in dollar-backed stablecoins.

Benefits of DeFi lending and borrowing?

Now that we have developed a better understanding of DeFi lending and borrowing and how it works, let’s take a look at some of its major benefits:

- Decentralization

- Global Accessibility

- Competitive Interest Rates

- Permissionless Access

- Liquidity Pools and Automated Market Making

- Transparency

Decentralization

DeFi operates on blockchain technology, eliminating the need for traditional intermediaries like banks. Smart contracts facilitate lending and borrowing directly between users, reducing counterparty risk. This decentralized nature fosters trustlessness and executes transactions automatically based on predefined conditions without relying on a central authority.

Global Accessibility

DeFi platforms are accessible to anyone with an internet connection and a compatible wallet. This inclusivity extends financial services to a global audience, including the unbanked or underbanked. Users worldwide can lend and borrow money because there are few restrictions based on location.

Competitive Interest Rates

DeFi lending and borrowing often involve competitive interest rates determined by market forces.

Lenders can earn attractive yields on deposited assets, while borrowers may access funds at rates that reflect supply and demand dynamics within the decentralized ecosystem. On the other hand, central authorities set interest rates in traditional financial systems.

Permissionless Access

DeFi platforms are generally permissionless, meaning users can participate without undergoing extensive KYC (Know Your Customer) processes.

This open and innovative environment allows for the creation of new financial products and services. Users can experiment with various lending and borrowing strategies, contributing to a dynamic and evolving ecosystem.

Liquidity Pools and Automated Market Making

DeFi lending often involves liquidity pools, where users contribute their assets to a shared pool. This contributes to increased liquidity, enabling borrowers to access funds more efficiently.

Automated market-making (AMM) algorithms adjust prices based on supply and demand, enhancing the efficiency of trading and lending pairs.

Transparency

All transactions on the blockchain are transparent, traceable, and immutable. Participants can verify the details of any transaction, enhancing transparency and accountability.

Smart contracts, the backbone of DeFi protocols, are open for scrutiny, allowing users to audit the code and understand the management of funds within the system.

Risks Associated With Lending and Borrowing In DeFi

While DeFi overcomes many shortcomings and reduces the risks associated with CeFi, it also poses its risks, which include:

- Flash Loan Attacks

- No Credit Scores

- Impermanent Loss

- Rug Pulls

- Smart contract

- Quickly changing APY

Flash Loan Attacks

Unique to the DeFi space, flash loans are uncollateralized loans given out to borrowers for a short time.

Unsecured loans that leverage smart contract functionality to reduce the risks associated with TradFi.

Flash loan attacks are scenarios where bad actors borrow huge amounts of money and use them to manipulate the market and exploit other DeFi protocols for personal gain.

No Credit Scores

Because the entire space is decentralized and permissionless, there is no concept of credit scores. This information can be vital for lenders’ safety, but at the moment, there is no such feature in DeFi protocols.

Impermanent Loss

When lenders provide liquidity to liquidity pools on DeFi platforms, they face the risk of impermanent loss.

This loss occurs when the price of an asset in the pool changes, and the lender loses value instead of holding the asset in their wallet.

Rug Pulls

As there is no regulation, users must trust protocols with their funds. Some DeFi developers misuse this trust and create rug pull scenarios, an exit scam. In 2020, one of SushiSwap’s founding developers liquidated all his SUSHI tokens to raise over a billion dollars in collateral.

Smart contract

Smart contract risks are ever-present in DeFi. Developers build protocols and smart contracts on codes; no code can be perfect.

Quickly changing APY

The quest to earn higher returns through yield farming motivates liquidity providers to quickly change liquidity pools and opt for the one offering the highest interest rate.

For example, once the borrowing APY on the BAT token on the compound protocol increased to over 40%, As a result, users who were not tracking the interest rates daily were at risk of getting liquidated.

Top DeFi Lending and Borrowing Platforms

Several DeFi lending platforms have gained prominence in the ecosystem. Each platform differs in interest rates, supported assets, and user experiences.

Users can choose the platform that aligns with their preferences and risk tolerance. The top lending and borrowing platforms are:

- Aave

- Anchor Protocol

- Compound

- Maker

- Venus

Aave

Aave was formerly known as ETHLend. In 2017, Stani Kulechov created it. Later, in September 2018, it was rebranded to Aave. ‘Aave’ is Finnish for ghost. The Aave logo also features a ghost, signifying no central authority governing borrowing and lending.

As we write this piece, the total value locked in Aave stands at $12.7 billion.

Aave supports borrowing and lending on multiple blockchains. It supports the most significant number of blockchains on any DeFi lending protocol.

Anchor Protocol

Anchor Protocol is a borrowing and lending platform that offers up to a 19.5% yield on deposits of stablecoin UST. Developed on the Terra ecosystem, it allows users to earn higher profits on their crypto deposits. Compare that to a savings account, which offers no more than 4% APY.

Daniel Shin and Do Kwon founded the South Korean fintech company Terraform Labs, which founded Anchor Protocol in March 2021. Terraform Labs is also behind the Terra layer-one blockchain that has taken the DeFi space by storm, rising by 17,000% in 2021.

Compound

Compound is the third-largest lending protocol by TVL in the DeFi ecosystem. This decentralized protocol lets users secure their assets in a smart contract. Yet again, it is developed on the Ethereum blockchain.

The compound is audited and regularly reviewed for security. A reserve keeps 10% of all the interest paid and uses the rest to repay liquidity providers or people who put money into the protocol.

Maker

This borrowing and lending platform has a unique approach. Maker works on a multi-collateral DAI (MCD) system. DAI is the stablecoin of the Maker protocol. Multiple assets pre-approved by Maker Governance backs this stablecoin.

This ecosystem has two main assets: MKR and DAI. DAO is a decentralized lending application on the Ethereum blockchain that supports the DAI, a stablecoin pegged to the US. It also lets users with access to ETH and MetaMask lend in the structure of DAI.

Venus

The Venus protocol is based on the Binance smart chain. It is an algorithmic money market with a synthetic stablecoin protocol. A unique selling proposition for Venus is that it enables users to minimize losses in transaction fees while allowing fast transactions.

Users can also instantly mint VAI (the stablecoin of the protocol) by depositing 200% of the collateral. Both VAI and XVS (Native protocol token) are BEP-20, making them much cheaper in terms of transactions due to lower gas fees.

$XVS is also a governance token that can be used to vote on various decisions like adding new collateral types, changing parameters like fees, etc., and setting priority on product improvement.

Conclusion

DeFi lending and borrowing represent a paradigm shift in the financial sector. The decentralized nature and innovative technologies open new financial inclusion and efficiency possibilities.

The decentralized finance ecosystem is growing and will continue to grow at a breakneck pace. It will try to make its services as good as existing centralized finance options, keeping the principles of decentralization and openness in mind.

However, this is a space that comes with an innate risk. Hence, users who want to avail of this functionality should ensure that they do their homework before they decide to put their cryptos into these DeFi protocols or even if they will take a crypto loan through DeFi.